Start Here

A guide to who I am, my qualifications, returns and philosophy

Hi and welcome to Edge!

My name is Armin, and I specialize in asymmetric value investments backed by data-driven insights.

If you are a new subscriber, or are considering joining, thank you for your trust!

I’ve compiled this guide because my approach requires explanation and nuance.

Like my investment posts, this guide is plain text and fully transparent with links to sources/references.

My goal is to give you a comprehensive understanding of how I work - and why I work this way.

Table of Contents

Who Am I and How Did I Get Here

What This Substack Is (Including My Incentives)

What This Substack Is Not

My Approach to Investing

My Hunting Ground

Useful Links (Case Studies and Past Representative Write-ups)

Closing Words and Disclaimer

Who Am I and How Did I Get Here

I began my career in M&A at a global top-tier investment bank before joining a first-quartile European mid-market Private Equity fund and, eventually, a mid-cap value hedge fund (LinkedIn Profile).

During my time in the industry, I worked on transactions exceeding EUR >1bn, worked closely with the management of a company generating several billions in revenue, and conducted due diligence across dozens of sectors - from green-tech industrial scale-ups to legacy software assets.

Despite learning from and working with high-performing investors, one thought kept me up at night: I can do even better (Oh, how humble of me!)

Thus, I started a side-hustle to find more compelling investments for my own savings. And it worked!

I generated a return of 36.2% p.a. (Link) without leverage, even while managing significant monthly inflows. This performance didn’t just beat the S&P 500, it outperformed my former employers.

Once it became clear that my process was repeatable, I could no longer justify working for anyone else. Today, I am an independent investor.

What This Substack Is (Including My Incentives)

If you’re doing so well, why do you run a Substack?

That’s a fair question! I believe incentives drive outcomes. To be transparent, here is my “Selfish Business Model”.

I obviously want to make money, and Substack helps. But not just via subscription fees.

In investing, Mr. Market only pays you for how sound your ideas are, not how many you have. I am constantly refining my process to favor quality over quantity.

Fundamentally, I believe that writing is thinking. Publishing my ideas forces me to be more rigorous, logical and honest about my own assumptions. Posting investment focused content makes me a better investor. That is the primary reason this publication exists.

Here’s a run down of my workflow. Substack fits into my “normal” investing process neatly:

Screen for compelling investment opportunities

Write a thesis to discover flaws in my line of thinking and white spots

Go back to due diligence and understand the investment better

Repeat until I can make a decision based on an improved information set

Invest my own money: At least 5% but up to 25% of my net worth

Publish a post based on the work I already conducted

Use Substack proceeds to improve the quality of my research by paying for expensive resources - like expert networks and data providers - and to fund further investments

My Substack is an extension of the research I would have done anyway!

Posting requires very little additional effort and doesn’t cost me a dime, but can generate unlimited upside. As investor, this asymmetric set-up is very enticing!

But there is more: The optionality to connect with like-minded investors. Whether it be immediately tangible like community discussions highlighting errors in my investment thesis, sharing ideas or vague optionality like marketing for capital allocators if I ever chose to open a fund in the future.

I can get all of this upside for a little bit of time and effort to make my research presentable? This sounds like one hell of a deal to me!

But with that it becomes also obvious what my Substack is not..

What This Substack Is Not

To manage expectations: This is not a traditional newsletter, and I am not your personal equity research analyst.

You won’t find weekly stock picks, primers on basic investment concepts, or constant engagement in a subscriber chat.

While providing a high volume of content would likely help me scale my subscriber count faster, it would also distract me from my most valuable task: finding compelling ideas and uncovering insights.

To be clear: This does not mean that there will never be weekly posts. In fact, I plan to post regularly, but just not new investment ideas.

I try to spend my time wisely by understanding companies, analysing industry dynamics and gathering data to either confirm or disconfirm beliefs. As I need to back my decisions with data from reputable sources, I’m slow to come to conclusions I believe to be sound. Let alone find something that is widely mispriced.

Maybe there are people who cracked the screening code and can deliver 1-2 truly good investments per month (all the power to them). I can’t do that!

I believe that there is a lot of noise in the Fintweet/Finstack bubble. Finding an interesting set-up and analysing it usually takes longer than a couple of days. And then there are the cases which started off interesting but became a pass. All of that happens regularly. A newsletter churning out weekly posts requires authors to publish anyway.

Not all of the creators are acting this way, but on aggregate there should be a not neglectable number doing so. I find little value-add in this posting strategy. But it is highly rewarded by the algorithm. To me, it’s much higher value if I only post new companies occasionally, but if I do, follow up with deeper industry analysis which are too time consuming for most other publications.

Don’t be wow’ed, these analysis would be required by any institutional investment committee worth their money. They are just not required for most Substack publications. A flow of new high level ideas apparently provides more than enough clicks.

I don’t blame these creators. I respect their hustle and they have qualities I clearly don’t possess. They are maximizing for the creator-game. Contrary, I am maximizing for the investment-game.

Both approaches have their reason d’être. I’m fine with my ‘randdasein’ (German word creation loosely translating into ‘existence on the sidelines’). From my point of view I’ve chosen the harder path as a creator, but the easier path as an investor.

My Approach to Investing

As initially said, this Substack is an extension of my own research. I have the vast majority of my net worth tied towards the companies I cover here. Money I can’t afford to lose.

Every person brings its own flavor to investing. I’m fundamentally aligned with the approach of value investors like Buffett, Munger, Greenblatt, Klarmann, Marks, Lynch, Akre - you name them.

The holy grail of investing is a capital-light compounder with high returns on incremental capital deployed, expanding moat and long growth-runway. Think about American Tower, Google or Mastercard twenty years ago. And of course the price paid for such assets shall be cheap, with a sizeable margin of safety to account for potential errors in the analysis.

The problem is that most investors are after these kind of assets and they are easy to identify. Thus, prices are sky high - and I don’t like to pay high prices, I’m a cheap skate.

Occasionally, compounders become available at attractive prices. But that’s rare. Maybe once a decade the market goes bonkers and offers compounders at a good deal.

So, what are we doing in the mean time? Well, hording cash and waiting for a once-in-a-decade crash is a lousy strategy. Instead, I look for unsexy businesses which are temporarily widely mispriced.

Understanding this is crucial! I’m after high-quality, durable compounders but not for every price. Until I get an attractive pitch, I’m more than happy to play a different game. And the game is finding low-downside with high probability of high upside. You can call it asymmetry, torque or skew - they all fit the bill.

And now comes the frustrating part for me and you alike. I don’t know where these opportunities hide or when they’ll show up. If I had a bulletproof way of forecasting this, I’d be a billionaire already.

One thing I know for sure is this: To increase the likelihood of finding attractively priced assets, I have to have an edge. Some advantage that competitors don’t have. I believe my advantages are:

Size: I (sadly and luckily) work with small sums of money. I can, but don’t have to, deploy cash in opportunities that are not accessible to most institutional investors

Thematic/niche freedom: I don’t need to follow a mandate, I can deploy cash in any geography, industry, asset class or capitalization range

Sizing: I’m not regulated and can go as big as I want in any holding

I don’t like constraining myself. Why should I only focus on small-caps if a mid-cap stock is irrationally cheap? Why only look at North American assets if something cheap is to be found in Europe? Why deploy only 2% in my highest conviction asset? I can continue but you get the point. Flexibility is a major asset.

Hence, my sourcing efforts take me to many weird niches as long as I think I can understand the assets. And this limits the pool drastically. Nevertheless, I value flexibility over a niche. But why are so few investors following this approach?

One of the best ways to raise a fund or grow a Substack channel is to focus on a niche. Becoming the guy for growth, small-caps, Asian equities, turnarounds, dividend stocks or any other theme you can think of. It’s easy for allocators/readers to think in specialization. Capital allocators, just like audiences, prefer to categorize in pre-defined niches and create their own portfolio of various pure-play strategies. The problem is that I’ve experienced in practice how bad an idea this is.

How many great ideas do you think exist in growth stocks at a given time? Or in European small-caps? The more narrow you go the less enticing your basket of stocks becomes - through the cycle. In the short-term each theme can explode. But as narrowly focused investor you are reliant on external factors, i.e. the theme exploding. Why not keeping optionality to “go fishing where the fish are” is beyond me. I believe that over the long-run it pays to be opportunistic.

This brings me to the seemingly weird collection of businesses in my portfolio. I’m not opposed to Australian nano-caps, Canadian media companies, capital light large-cap software players, capital intensive mining companies, O&G exploration, nor critical infrastructure. The one common thread? The assets are priced at a large discount to intrinsic value which I expect to narrow in the medium-term.

My niche - if you want to call it like that - is easy to understand, predictable assets with a low risk of permanent capital impairment but multibagger potential. My hurdle rate is a 2x in 3 years, 3x in 5 years or 10x in 10 years - roughly a 26% CAGR.

My Hunting Ground

I’m a sports-fanatic and avid admirer of the all time greats. It doesn’t matter which sports icon you cheer for. Whether it’s Brady, Federer, Phelps, Ryan (sneaky BJJ reference), Schumacher, Messi, Woods, the common theme is an obsession with process.

Of course we see the same thing with the great investors. Part of their process, especially in the early phases of their career, was a ruthless focus on their edge. The early Buffett and Greenblatt averaged ~50% p.a. for a decade.

For someone focused on an improved process, it’s only logical to look at those investors’ approaches and implement leanings. To find an edge, I go where the competition is thin and expected returns are high, focusing on:

Thinly covered small-caps

Un-loved / non-ESG conform industries

Recently heavily sold-off companies/industries

Embedded assets if management is planning an unlock

Special situations (Spin-offs, merger securities, restructurings)

Options (very rarely and only for companies I have a fundamental view on)

Finding the idea is just the start, execution is even more important. Besides the selection of assets, sizing appropriately is a key driver of returns. I only have so many hours to research ideas, when I find conviction in one the sizing has to be adequate.

I consider an exposure of 15% of cost basis not too aggressive. Historically, I initiated at a 10% exposure. New contributions and anchoring bias led to a cash cushion and only one bet with exposure exceeding 15%. After reflection and studying how investors I admire approached sizing, I landed at 10-15% for new positions.

Useful Links

All this theory is nice, but decisions are best made with evidence. If I’d consider subscribing to a channel I’d wanted to know the authors track-record, selective investment write-ups, and other representative posts similar to future posts.

That’s exactly what you’ll find below.

Track Record and Exited Investments

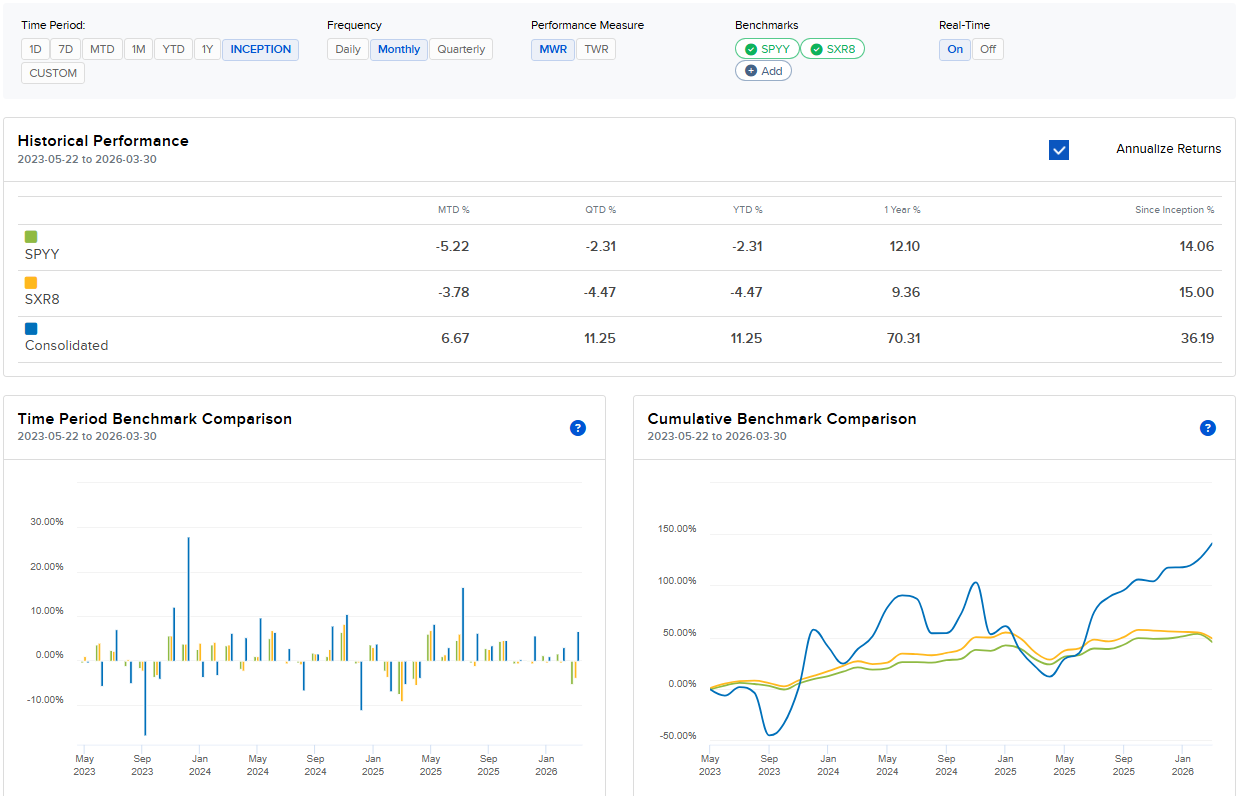

I started investing my own money during the fall of 2022 and have an IBKR account since May 2023. Since using IBKR I generated twice the S&P 500’s return, compounding at a rate of 33.9% p.a. (as of Feb-2026). I publish my returns monthly for full transparency.

In one of my early posts, I provided a walk-through of every investment I made to this date. I continue to hold Shopify and Prosus and discussed in length why I believed Hindenburg’s short-report on Carvana lacked evidence. I eventually exited the position after the stock rallied >60% following the S&P 500 inclusion, trading at >100x P/E. I locked-in a 4.5x in less than 2 years.

One past investment I want to highlight is in a company called Falcon Metals as it presented a set-up I can imagine using more frequently. It’s rare but exactly the hidden nano/small-cap ideas that are not worth the while of institutions:

Falcon Metals (+176%): FAL.AX is an Australian nano-cap that engages in gold exploration. In 2024, they encountered a large deposit of heavy mineral sand. They disclosed enough information to triangulate minimum volume for the deposit, average % heavy mineral sand content and market prices for the commodities. It only required a little bit of basic math to estimate the value of this deposit, which came out to be at a conservative ~3.5x their market cap. This seemed interesting, especially since Falcon had other project as well which provided free call options on additional value. Would have someone told me that I will realize 2.8x in less than 1 year, I would be thrilled, but it turns out that there are valuable lessons and harsh realizations about how to manage my emotions going forward. (…)

Company write-ups

Besides a thesis as simple as Falcon, I like looking at special situations that are fundamentally simple, but require significant digging. Blue Ant Media is such a situation. The underlying economics are hidden because mergers created a confusing construct that have not yet revealed as the first report with consolidated numbers is still some weeks away. The thesis was that a liquidity crunch from motivated sellers would depress the price, offering an enticing entry. So far, the plan is on track; we are simply waiting for the catalyst.

![[BAMI.TO] Blue Ant Media | Hidden Economics Offering 3x Upside](https://substackcdn.com/image/fetch/$s_!X6GD!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F0f7f9bd8-c703-4cbe-a0ce-24554566498d_1456x1048.png)

When a case rests on capital allocations and there are roadblocks that are covered in fine print or dense legislations, I believe it warrants a deep dive. I spent significant time translating the complexities of Warrior Met Coal into plain English, as it directly impacts one of my core holdings.

![[$HCC] Warrior Met Coal's Buyback Dilemma](https://substackcdn.com/image/fetch/$s_!nr-S!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Ff10408ff-7cf0-49a2-aa2d-126c3989ca16_1456x1048.png)

Sometimes it’s enough to recognize that the sum-of-the-parts don’t match the company value. This is a similar thesis as with Falcon. The write-up of course covers important industry backdrops, relevant comps to anchor the valuation and an evaluation of risks.

Industry Analysis

Not every industry can be easily analysed in great depths given a lack of data. The offshore rig industry is different. There’s not only freely available information, it is also heterogeneous and dispersed. I figured a homogeneous, consolidated view on the data would be instructive in judging the industry.

![Offshore Drillers | Q4 2025 Market Round-up [$RIG $VAL $NE $SDRL]](https://substackcdn.com/image/fetch/$s_!c5K3!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fa0711ba3-ff34-4b56-a976-c857c1a852bb_1456x1048.png)

Looking more deeply into met coal was also very insightful. However, the focus here was on benchmarking of the players as being the low-cost producer is imperative in a cyclical industry.

Closing Words and Disclaimer

I hope it became apparent that I value insights and high quality of investing. That’s the sole reason I structure my content the way I do. It should allow for the best possible research, thus eventually providing you with the most value.

There might be weeks you don’t hear anything from me, but that’s not because I’m not working on uncovering insights for us, but because I don’t think that what I found is worth your while. Instead of reading my gibberish, spend the time with your family or friends. Eventually, there will be a time I believe my words are worth reading. Then I hope they’ll grab your attention.

Disclaimer:

While I try to highlight interesting companies, I want to be very clear: My content does not constitute investment advice or any other sort of advice. No post should be construed as a personal recommendation or advice to buy, sell, or hold any investment or security. All content is provided for general informational purposes only and should not be relied upon for making investment decisions.

I may own (or short) securities mentioned and may change positions at any time without notice. Investing involves risk, including loss of principal. Do your own research and consider speaking with a licensed adviser who knows your financial circumstances, investment objectives and risk tolerance.

Thank you for reading!

Armin